Our products are built on over 15 years of applied research in operational risk. MSTAR Desktop is our core tool for designing and simulating risk scenarios. MSTAR Platform includes a curated news feed and a library of operational risk scenarios, and can be fully customised for internal deployment.

These tools are trusted by leading financial institutions for scenario-based risk analysis and regulatory use cases.

MSTAR Desktop

Core Tool

Design and quantify risk scenarios. Built-in Python, R and Matlab export for integration into external applications.

MSTAR Platform

Award-Winning

40+ curated scenarios updated quarterly, dynamic dashboard, real-world news feed. Risk.net Award 2020.

MSTAR app

Operational risk news and scenario library on iOS & Android. Free to download.

product 01

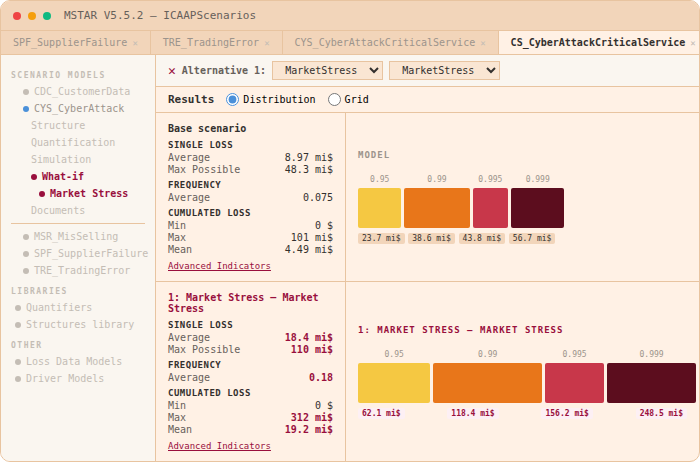

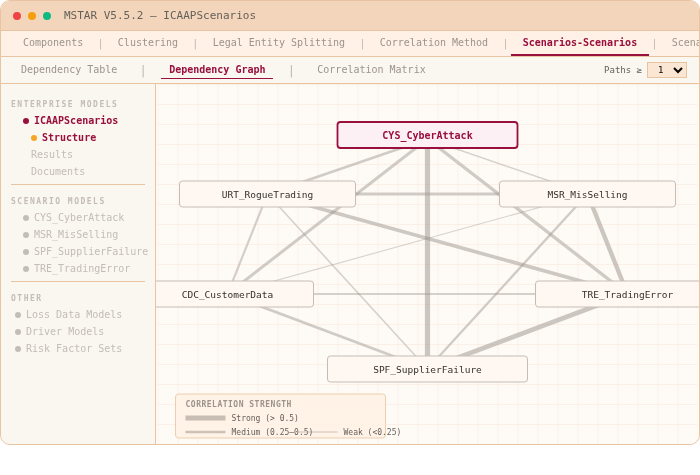

MSTAR Desktop: Oprisk Scenario Design

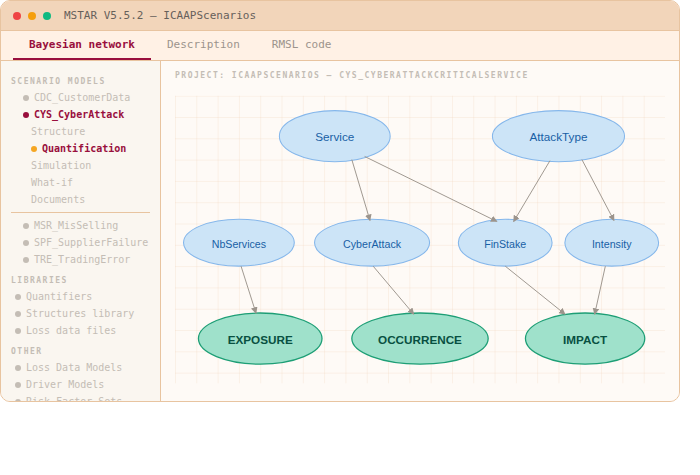

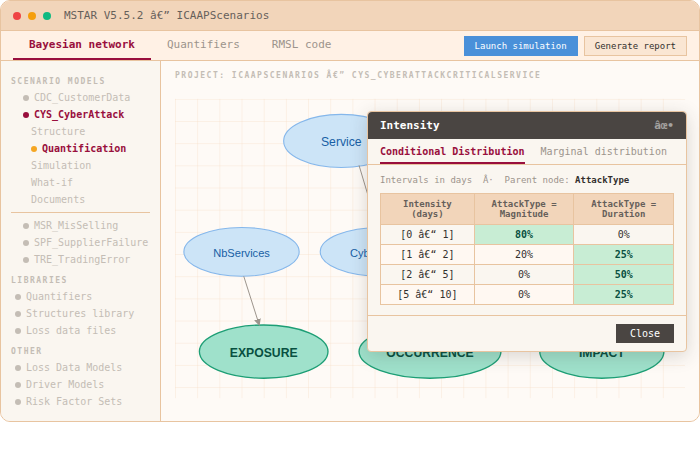

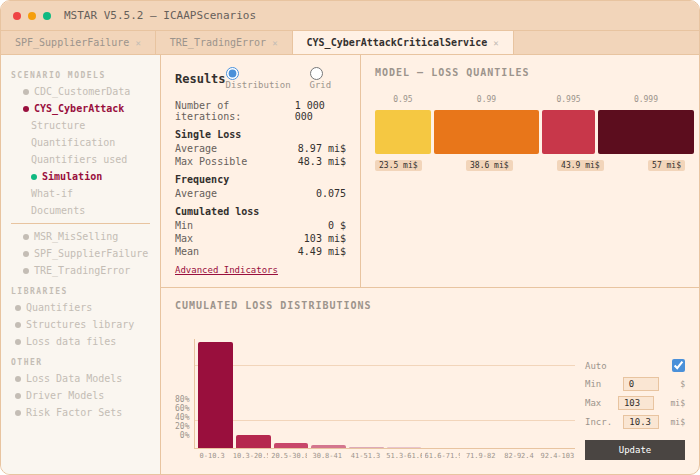

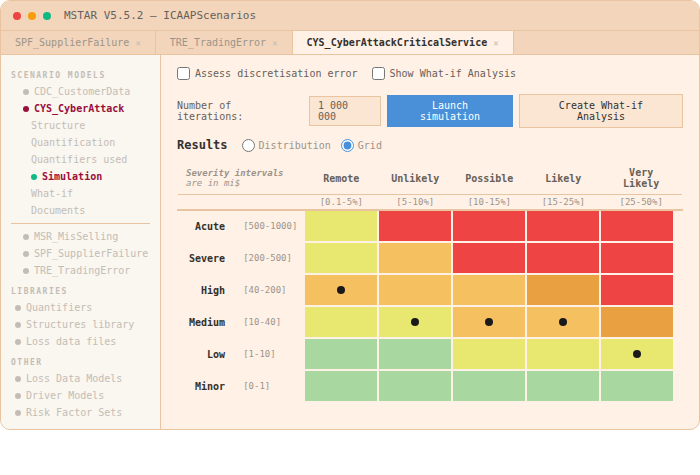

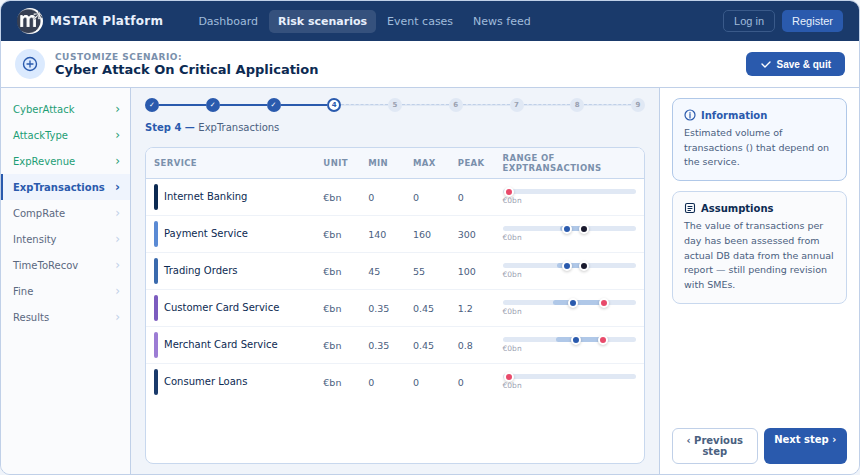

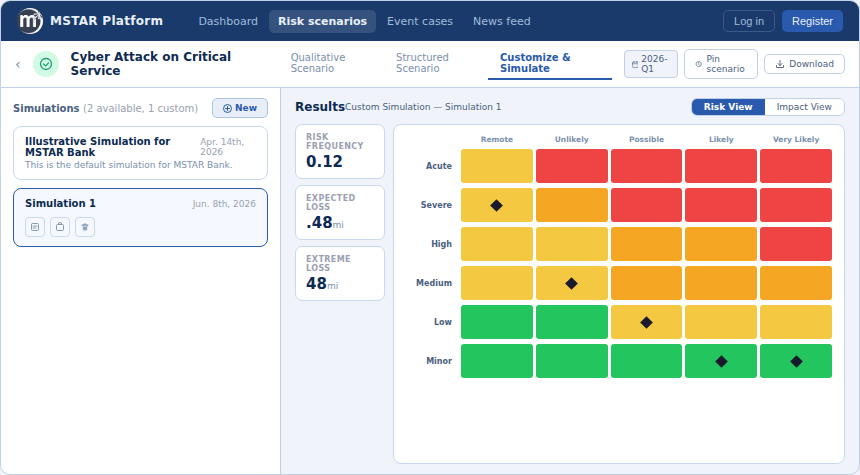

MSTAR Desktop implements the XOI method for designing and quantifying your own risk scenarios, from

rogue trading to natural disasters by identifying exposure, assessing occurrence probabilities, and calculating impacts.

MSTAR Desktop can also generate simulation scripts in Python, R, or Matlab for integration into external applications

MSTAR Desktop can also generate simulation scripts in Python, R, or Matlab for integration into external applications

Download Trial

product 02

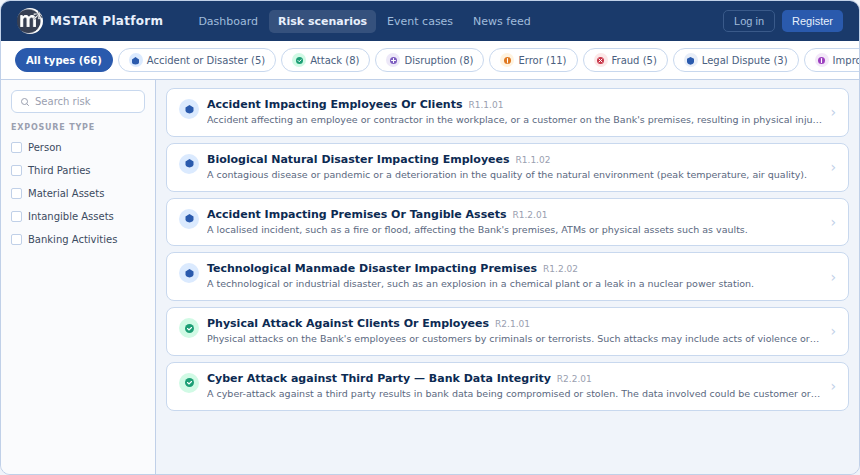

MSTAR Platform: Oprisk Scenario Library

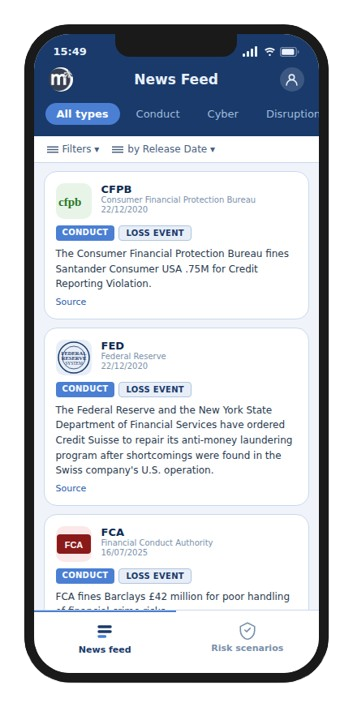

The award winning MSTAR Platform (Risk.net 2020) offers a free curated news feed linking real-world events to our risk scenarios.

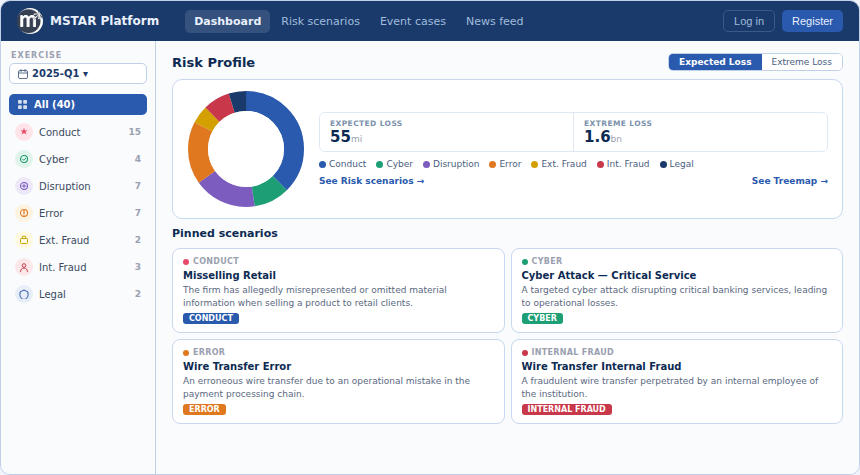

Subscribers unlock a comprehensive library of 40+ operational risk scenarios across Conduct, Cyber, Errors, and more.

With the Enterprise platform (on-premise), everything can be fully customized to your organization’s needs.

Register for Free

Subscribers unlock a comprehensive library of 40+ operational risk scenarios across Conduct, Cyber, Errors, and more.

With the Enterprise platform (on-premise), everything can be fully customized to your organization’s needs.

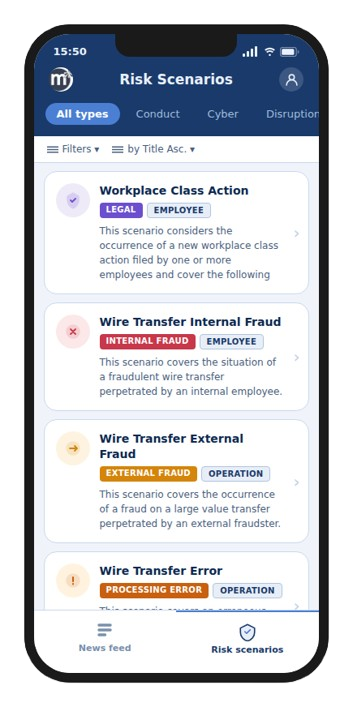

MSTSR App

News & Scenarios on iOS & Android

Live News Feed

Stay updated on operational risk events globally.

Scenarios Library

Access 40 scenarios of all risk types: Conduct, ESG, Cyber, Fraud, Error, Disruption, and Legal.

Download on the App Store

Ready to Transform Your Approach to Operational Risk?

Our experts are available to assess your needs and provide a personalised demonstration of MSTAR.

Try MSTAR DESKTOP FOR FREE

Download

MSTAR Trial

Please fill out the form to receive the software and license file. The license will be valid for 1 month.

By submitting this form, you confirm that you agree to the storing and processing of your personal data by Elseware as described in our Privacy Policy